Medical imaging technology has transformed healthcare market enabling doctors to detect diseases earlier and develop curable outcomes. It has been used by various medical end users such as hospitals and diagnostic imaging centers. Medical image management refers to the managing medical images electronically by image management systems. Management of medical images includes the need for integration with a variety of information systems. These information systems help in managing, controlling and storage of imaging data and patient information in the health care system. Global medical image management market is estimated to have 6.5% of CAGR during the forecast period 2016-2023. The key trend affecting the market is the increasing adoption of new technologies such as cloud technology, 3D mammography, multimedia enhanced radiology reporting and tetelemedecine. The benefits from these five key technology trends in medical imaging become more extensive. This new technology upgradation in medical imaging devices will enhance the efficiency and effectiveness in diagnosis and treatment.

Global medical image management market is primarily driven by following factors:

- Increasing usage in imaging centers and small hospitals

- Increasing innovations Government support for encouraging Electronic Medical Records (EMR) adoption,

- Increasing investment in healthcare IT technologies

- Growth in cloud based solutions

The major factor affecting the market demand is government support for encouraging EMR adoption. The HITECH Act (The Health Information Technology for Economic and Clinical Health Act) determined that it can applicable for $44,000 and above for the adoption of EMR or EHR in economic stimulus incentive payment. The government distributed $27 billion dollars to encourage doctors to shift from traditional (paper) medical records to EHR (Electronic health records) or EMR (electronic medical records). EHR & EMR incentives are funded per provider. The incentives provided under the HITECH Act encourages physicians or doctors to adopt the EMR & EHR systems and thus, it is a major driving force for global medical image management market.

The market has some restraining factors such as budgetary constraints and concerns in post implementation of VNA and the challenges faced by the market are lack of adept personnel to maintain VNA solutions and strict adherence of VNA to open industry standards such as HL-7 & DICOM. The market has lot of opportunities with the combination of VNA/PACS with ECM/EMR and rising adoption of PACS & VNA.

Source: OBRC Analysis.

The global medical image management market segments includes products and end user. Products is further segmented into:

- Picture archiving & communication system (PACS)

- Vendor neutral archives (VNA)

- Application-independent Clinical archive (AICA)

End –user is further segmented into:

- Hospitals

- Diagnostic imaging centers

- Others (contract research organizations, small clinics, etc.)

The revenue for the above end users is specific to the advanced visualization market. However, the total revenue of these end-users in general has been excluded from the scope of the report. Also, the total market revenue has been calculated by summing up product segment.

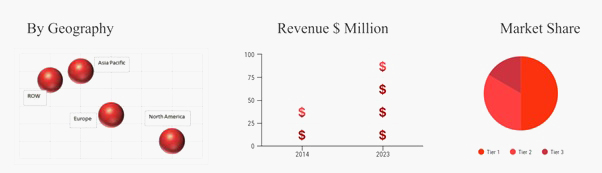

Geographically, the global medical image management market is segmented into:

- North America (U.S. & Canada)

- Asia Pacific (China, India, Japan, RoAPAC)

- Europe (UK, France, Germany, RoE)

- Rest of World

North America is leading the global medical image management market because U.S. holds the major share of the market. Americans aged 65 and above is expected to reach up to 98 million by 2060, and the share of 65 and above age group in the total population will increase to approximately 24% as compared to the current 15% in US. Europe and Asia Pacific are also the major regions of global medical image management market. European medical image management market is enhancing due to the increasing cases of diseases such as CVD & cancer. WHO stated that the number of deaths caused due to CVD is 46 times the number of deaths and 11 times the disease load caused due to malaria, tuberculosis and AIDS in Europe. Asia Pacific has great opportunities for the market with the rising awareness among people regarding the early identification of diseases. The maturity of the region is increasing due to growth in healthcare system. Both Taiwan and Korea have started national health insurance schemes that cover approximately majority of the population. Thus, the introduction of these type of systems are encouraging people regarding medical care services

The global medical image management market is segmented on the basis of end users and product. According to end user, the market is further segmented into diagnostic imaging centers, hospitals and other end users such as contract research organizations, small clinics, etc. Hospital segment held the major share of the medical image management market in 2015. The growth in patient population, rising digitization of patient information, technological innovations in imaging modalities, rise in diagnostic imaging, increasing EMR adoption and rising awareness about the advantages of early identification of diseases are the key factors accountable for the major share of hospitals in the market. According to product, the market is further segmented into Picture archiving & communication system (PACS), Vendor neutral archives (VNA) and Application-independent Clinical archive (AICA). PACS is again sub-segmented into enterprise PACS and departmental PACS.In 2016, the PACS segment was expected to hold the major share due to growing adoption of PACS in the novel imaging segments such as oncology, mammography, endoscopy and ophthalmology.

The major market players of the global medical image management market are:

- GENERAL ELECTRIC COMPANY

- CARESTREAM HEALTH

- HITACHI DATA SYSTEMS

- PHILIPS HEALTHCARE

- SIEMENS HEALTHCARE

- OTHERS

Detailed analysis of these companies provided in this report comprises of overview, SCOT analysis, product portfolio, strategic initiative and strategic analysis.

The company use various strategies such as mergers & acquisitions, product launches, partnership etc. to expand market share globally. For example: On May 2015, Fujifilm acquired TeraMedica, Inc., the U.S. healthcare IT software company to enhance its healthcare IT business. The acquisition enabled Fujifilm to develop the quality of medical care services. Fujifilm merged with TeraMedica’s VNA with its series of information systems to provide solutions that supports medical diagnosis with higher efficiency than ever before.

Why to buy the report:

This report will:

- Provide you the business strategies adopted by market player such as acquisition as in May 2015, Fujifilm acquired Tera Medica, Inc., the U.S. healthcare IT software company to enhance its healthcare IT business.

- Provide in detail the different segments such as products and end-users which affect the global medical image management market.

- Provide you the patent analysis of global medical image management market.

- Identify and understand the strengths, opportunities, challenges and threat of the medical image management market.

- Provide revenues of major players of the market such as GE Company (U.S.), Fujifilm Holdings and Siemens.

- Provide you the various regulatory policies which affect the global medical image management market.

How we are different from others:

At Occams we provide an extensive portfolio which is comprehensive market analysis along with the market size, market share, and market segmentations. Our report on global smart security market offers the longest chain of market segmentation covering major market segmentation based on products and end users. The report tracks the major market trends in the global medical image management market such as new technology advancement in medical imaging industry for example remote viewing systems and adoption of cloud technologies. For each market segments covered in global medical image management market report, we provide opportunity matrix, and DROC analysis, that enable the clear growth assessment across each market segment. The report discusses competitive landscape of the smart medical image management industry, with giving extensive strategy analysis of more than 15 companies. Moreover, the report discusses various models such as 360 degree analysis, See Saw analysis, and Porter five force model and so on. For the high level analysis in the report we provide a comparative analysis of historic and current year data.

Key findings of the global medical image management market:

- North America had the largest revenue share in 2016.

- PACS segment is dominating the market due to increasing adoption of PACS in the novel imaging segments such as oncology, mammography, endoscopy and ophthalmology

- Acquisition is the key strategy adopted by the various market players of global medical image management market.

- Hospital segment held the major share of the medical image management market in end-usersegment due to growing patient population, rising digitization of patient information and technological innovations in imaging modalities.