Clinical Decision support systems (CDSS) are fully computerized information systems which are designed to manage healthcare systems. The CDSS use patient’s information to provide evidence about them to health providers, which provide better summery reports. Global clinical decision support systems market is expected to have the CAGR of 12.2% during the forecast period 2016-2023. Due to the increasing number of chronic cases such as asthma and multiple sclerosis and diseases like cancer and diabetes, the global clinical decision support systems market is expected to grow. According to World Health Organization report, cancer cases are expected to reach up to 15 million by 2020. More than half of the deaths attributable to high blood glucose occur before the age of 70 years. As per WHO estimation diabetes will be the 7th leading cause of death by 2030. Such high number of cases would increase the demand of integrated form of healthcare provisions which are best managed by clinical decision support systems. CDSS leads to more safe, planned, efficient and effective medical decisions.

Global clinical decision support systems market is primarily driven by the following factors:

- Increasing government support

- High occurrence of chronic diseases

- Increasing incidence of medication blunders

- Increasing usage of big data and m-health tools

- Increasing adoption of cloud computing in healthcare

The increasing popularity of clinical decision support systems (CDSS) in healthcare sector is the major factor driving the global CDSS market with other factors such as high capital expenditure and maintenance requirement, privacy and security issues, and inadequate healthcare infrastructure. Chronic diseases such as chronic obstructive pulmonary disease (COPD), cardiovascular diseases, diabetes, and cancer with the rising effect of harmful use of alcohol, smoking, poor nutrition and physical inactivity is also increasing the demand for better medical decisions. Innovation and technological advancement helps in creating a higher productivity for businesses and helps them to launch varied goods and services. It also enhances the internal part of production process at upward stage. Medical science has advanced exponentially during the last half of a decade. The paper system has hindered the capability to access the information vital to the delivery of care. On the basis of a survey, $600 billion is invested on lab tests each year in the U.S., out of that, 70 percent of the money pays for paperwork. Increasing service cost in healthcare industry has become a major challenge for every country, that’s why IT has now entered in the healthcare industry. IT provides quality based products and services to maintain all the information about patients and also reduces overall cost. The current condition of physical infrastructure of healthcare systems and their staff members reflects the requirements in infrastructure and services in the industry. Lack of adept IT professionals in the healthcare industry and rising complexity of the health sector and servicing organizations is a major challenge to be faced. Mainly, the problem arises in the underdeveloped general public health systems, inadequate medical training and service delivery.

Source: OBRC Analysis.

The global clinical decision support system market segments include type, product, model, user interactivity, application, component and delivery mode. Type is further segmented into:

- Therapeutic clinical decision support systems,

- Diagnostic clinical decision support systems

Product is further segmented into:

- Standalone clinical decision support systems,

- Integrated clinical decision support systems,

Model is further segmented into:

- Knowledge-based clinical decision support systems,

- Non-knowledge-based clinical decision support systems

User interactivity is further segmented into:

- Passive clinical decision support systems

- Active clinical decision support systems

Application is further segmented into:

- Conventional clinical decision support systems,

- Advanced clinical decision support systems

Component is further segmented into:

- Software

- Hardware

- Services

Delivery mode is further segmented into:

- Cloud-based clinical decision support systems,

- On premise clinical decision support systems

- Web based clinical decision support system

The revenue for the above industrial verticals are specific to the clinical decision support system market. However, the total revenue of these application in general has been excluded from the scope of the report. Also, the total market revenue has been calculated by summing up type, product, model, user interactivity, and application, component and delivery mode segments.

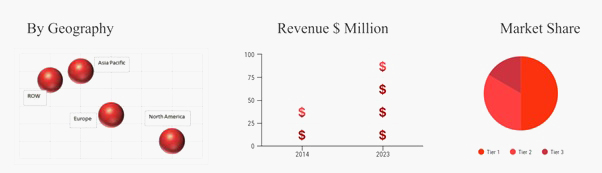

Geographically, the global CDSS market is segmented into:

- North America (U.S. & Canada)

- Asia Pacific (China, India, Japan, RoAPAC)

- Europe (UK, France, Germany, RoE)

- Rest of World

North America is anticipated to account the largest market share and the fastest growth rate during the forecast period 2016-2023 due to the increasing cases of diseases, favorable policies framed by the government and the adoption of information technology. Asia pacific region is expected to show the highest growth rate due to the rising focus on improving healthcare infrastructure, rising adoption of advanced technologies and increasing government funds and initiatives to improve health care industry.

The global Clinic Decision Support System market is broadly segmented on the basis of component that is software, hardware and services. Delivery mode is further segmented into web-based clinical decision support systems, on- based clinical decision support systems; cloud- based clinical decision support systems. Product is further segmented into standalone clinical decision support systems, integrated clinical decision support systems. Type is further segmented into therapeutic clinical decision support systems, diagnostic clinical decision support systems. Model is further segmented into knowledge-based clinical decision support systems, non-knowledge-based clinical decision support systems; User interactivity is further segmented into passive clinical decision support systems, active clinical decision support systems. Application is further segmented into conventional clinical decision support systems, advanced clinical decision support systems, and geographically. In 2016, the software segment had the highest growth rate during the forecast period due to the need for periodic software upgradation. The market for cloud-based CDSS solutions is anticipated to register the highest growth rate in the upcoming period. Some additional functions such as assisting clinicians in real-time evidence based decision making, population health management, treatment planning, financial decision support, and protocol validation among others, advanced CDSS segment is projected to grow at the highest rate in the forecast period. Through built-in reference table, treatments, containing inbred information about different diseases, and other constraints which decreases clinical errors and aid in treatment planning, knowledge-based CDSS segment is expected to control the largest share of the global market and is projected to grow at the fastest rate in the forecast period.

The major market players of the global clinical decision support systems market are:

- ALLSCRIPTS HEALTHCARE SOLUTIONS INC

- CERNER CORPORATION

- ZYNX HEALTH INCORPORATED

- INTERNATIONAL BUSINESS MACHINE CORPORATION

- SIEMENS AG

- OTHERS

These companies use various strategies such as merger & acquisition, collaboration, partnership and product launching. Example: In April 2017 Siemens Healthineers are expanding its health management portfolio by acquiring Medicales which is a leading company in clinical decision support solutions. Through this acquisition the company will be benefited by medicalis expertise and going to provide clinical decision support system to health systems.Theacquisitionhelpsin optimizing utilization and departmental clinical workflow and thus extending the Siemens Healthineers strategy to give value based health care.

Why to buy the report:

This report will:

- Provide you the business strategies adopted by market player such as product launch as in April 2017 the Siemens Healthineers is expanding its health management portfolio by acquiring Medicales of U.S.

- Provide in detail the different segments such as products, type, component, application, delivery mode, user interactivity and model which affect the global clinical decision support system market.

- Provide you the patent analysis of global clinical decision support system market.

- Identify and understand the strengths, opportunities, challenges and threat of the clinical decision support system market.

- Provide revenues of major players of the market such as General Electric Company, McKesson Corporation, and Wolters Kluwer

- Provide you the various regulatory policies which affect the global clinical decision support system market.

How we are different from others:

At Occams we provide an extensive portfolio which is comprehensive market analysis along with the market size, market share, and market segmentations. Our report on global decision support system market offers the longest chain of market segmentation covering major market segmentation based on products and end users. The report tracks the major market trends in the global smart security market such as development in video surveillance technology, content management, adoption of home cloud solutions and so on. For each market segments covered in global smart security market report, we provide opportunity matrix, and DROC analysis, that enable the clear growth assessment across each market segment. The report discusses competitive landscape of the smart security industry, with giving extensive strategy analysis of more than 15 companies. Moreover, the report discusses various models such as 360 degree analysis, See Saw analysis, and Porter five force model and so on. For the high level analysis in the report we provide a comparative analysis of historic and current year data.

Key findings of the global smart security market:

- North America had the largest revenue share in 2016.

- Software segment is dominating the market due to the need for periodic software upgradation.

- Acquisition is the key strategy adopted by the various market players of global CDDS market.

- The market for cloud-based CDSS solutions is anticipated to register the highest growth rate in the upcoming period.